This is the website of Dr Emilie J. Rutledge who, with almost two decades’ worth of experience in managing, designing and delivering university-level economics courses, is currently Head of the Economics Department at The Open University.

erutledge.com

Dr Emilie J. Rutledge

Emilie has published over 20 peer-reviewed papers and is the author of “Monetary Union in the Gulf.” Her current research focus is on employability, the feasibility of universal basic incomes and, the oil-rich Arabian Gulf’s economic diversification and labour market reform strategies. On an ad hoc basis, Emilie provides consultancy on developing interactive university courses, alongside analytical insight on the political-economy of the Arabian Gulf.

I have updated the Arabian Gulf datasets page. The Tables, Charts and accompanying notes I’ve added there, resulted from the research I undertook whilst writing a short piece for The Conversation, titled, “The Middle East conflict has swiftly exposed economic vulnerability in the region” and filed here as, “Epically Furious.”

An Iranian woman holding a poster depicting Iran’s Supreme Leader Ayatollah Ali Khamenei walks under a large flag during the 47th anniversary of Iran’s Islamic Revolution, on February 11, 2026 (a Majid Asgaripour/West Asia News Agency photo).Iranian school-aged girl depicted (an Adams Carvalho illustration).Arleigh Burke-class guided-missile destroyer “USS Delbert D. Black” fires a Tomahawk attack missile in support of operation “Epic Fury,” February 28, 2026 (a U.S. Navy photo).

Tomahawk attack

Regarding the 2026 Minab school attack, this is what we do know: on 28 February 2026, the first day of the America and Israel’s war on Iran, the Shajareh Tayyebeh girls’ elementary school in Minab (southern Iran) was destroyed by a missile attack/strike (words matter, take your pick). Iranian authorities told the New York Times that the attack killed at least 175 people, including scores of civilians. Human Rights Watch reviewed lists with dozens of names of children and adults reportedly killed in the attack, and was able to immediately match some names with ages and other identifying information on body bags and caskets.

Shajareh Tayyebeh school in Minab, Iran, February 28, 2026 (a Abbas Zakeri/Mehr News Agency photo).

The New York Timesreported that the investigation found that the attack was the result of a targeting mistake by the US military, which was carrying out strikes on an Islamic Revolutionary Guard Corps naval base of which the school building had previously been a part. The report said that US Central Command officers created the target coordinates for the strike using outdated data provided by the US Defense Intelligence Agency.

A compilation of images showing fragments of an American made missile and the bombed Iranian girls’ school in Minab (an IRIB photo).

Four avenues of investigation regarding the Tomahawk attack on Minab Girls School are provided here (the fourth has great satellite imagery of the site):

Graves being dug for children killed in deadly strike school in Minab (an Iranian Press Center/AFP photo).Poignant Petals (an Amirhossein Khorgooei/AP photo).

It is hard not to conclude that Iran was blatantly betrayed twice by the U.S. administration.

Betrayal 1

Oman and Tehran were fooled once back in June of 2025.

Betrayal 2

In a laudable and concerted effort not to be fooled for a second time, on February 27th Oman’s Foreign Minister, Badr Albusaidi, got on a plane and flew all the way to Washington D.C. and immediately went on to CBS’s flagship “Face The Nation” program to tell the American public directly that the concessions Iran had just offered to give to Trump were game changing and (Iranian) regime saving. Albusaidi—on behalf, I would ague, of all GCC countries—was doing his utmost to ensure that conflict would not break out, at least not over that weekend. After all, could he categorically guarantee that Messrs Kushner and Witkoff (Trump’s self-appointed diplomatic duo) would not possibly forgot to convey the message to the American people themselves? I would argue too that the Iranians themselves genuinely believed that the seismic concession that they’d just offered was enough to have at least forestalled any prospect of war braking out that weekend. If they had not genuinely believed this, there is no way that Ayatollah Ali Khamenei would have been where he was that morning with both his key advisors and members of his nuclear family around him—his primary residence in the heart of Tehran in broad, early Spring, morning daylight.

Betrayal 3

This I argue (here and elsewhere) is America’s betrayal of the long loyal oil-rich Arabian Gulf countries.

I am certain that the Gulf countries themselves will not have been happy that despite all their protestations — both on TV and behind closed doors — the Americans went ahead and for a second time attacked Iran without warning and without imminent threat. The special relationships that the leaders of Saudi Arabia, Qatar and the UAE had forged with Trump—furnished and oiled so-to-speak, with staggeringly large investment into America and the purchasing of U.S.-made military industrial equipment deals—appeared to have no influence on Trump’s decision to subject the region to another purpose-wise, ill defined war. The betrayal (of trust, friendship) was all the greater to the GCC countries because over the past decades they had spent billions upon billions on American armaments, withstood some domestic disquiet in offering to host and mostly cover the costs of American military bases on all six of their territories and indeed, a few of this countries had even signed up to Trump and Kushner’s Abraham Accords. The Gulf countries are right to feel aggrieved as the “safe haven” they had worked so hard to achieve was partly underwritten on the assumption that having an American presence in the background on their soil and at their ports, would prevent not provoke attacks.

Smoke rises from Sharjah City in the United Arab Emirates (an Altaf Qadri/AP photo).

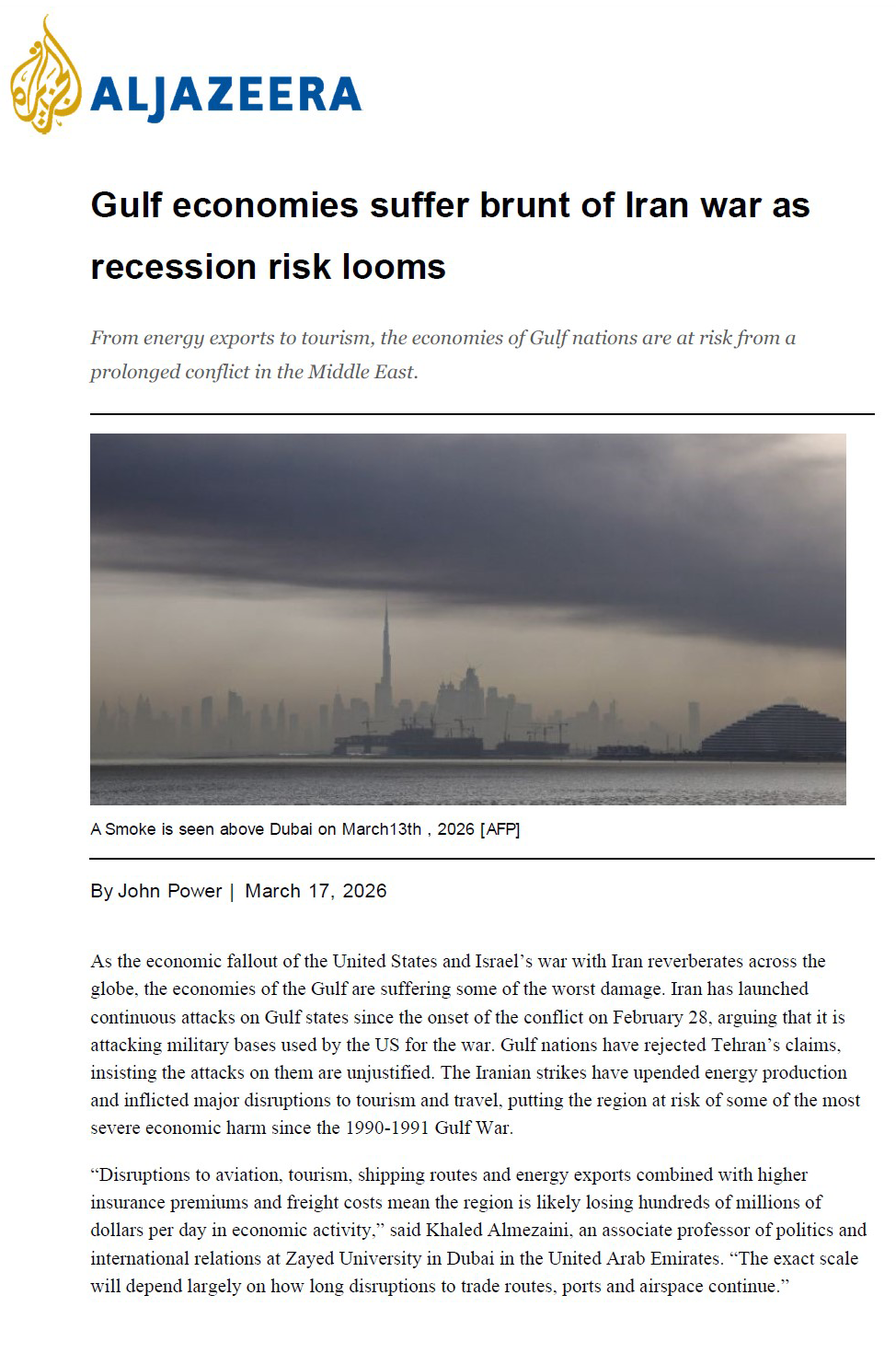

At the end of 2025, the Gulf states received high praise for their economic resilience. According to reports by the World Bank and the World Economic Forum, the region was stable, modern and reliable.

Now the six countries of the Gulf Cooperation Council (GCC) – Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates – are watching on nervously. The economic damage done by what has become a regional conflict, bringing an abrupt loss of stability, could be huge.

Aside from Saddam Hussein’s foray into Kuwait in 1991, these six countries have successfully steered clear of conflict on their home turf over a long period. They avoided the revolutionary upheavals which affected Egypt (1952), Iraq, Syria and Iran (1979). They steered clear of any spillover from the long-running Israel-Palestine conflict.

The group was mostly unaffected by the war between Iran and Iraq. And aside from a short-lived uprising in Bahrain in 2011, the GCC emerged largely unscathed from the regional turmoil of the Arab Spring in 2010 which spread from Tunisia and and Egypt and led to violent instability which continues to this day in Libya, Yemen and Syria.

The GCC’s comparative stability underpins its attractiveness as a global hub for money and modernity. Success in luxury tourism has filled places such as Dubai and Abu Dhabi with five (and even a seven) star hotels. Only France has more Michelin-starred restaurants than the United Arab Emirates (UAE). There is cutting-edge technology in Qatar’s energy sector, and a vast AI campus in the UAE.

It is these kinds of projects which led the World Bank and the World Economic Forum to publish glowing reports on the region recently. Both organisations agreed in late 2025 that oil wealth was being wisely invested for the future.

The general view was that the GCC was a place of economic stability and diversity. A director of the World Bank, Safaa El Kogali, said that the region’s embrace of a digital future had been nothing short of “remarkable”.

Missiles from Iran directly hit three Amazon web service facilities, one in Bahrain and two in the UAE, leading the company to recommend that GCC businesses back up their data and migrate it to data centres in the US.

Despite efforts to diversify economies away from oil, for now the region is still clearly dependent on oil exports and food imports, hence the worries over Hormuz. There are fears for its numerous desalination plants, which provide drinking water (as well as filling infinity pools and keeping golf courses green).

And its status as a safe and sunny sanctuary for conference conveners, influencers, holiday makers and owners of second homes is now being questioned.

Even if the conflict were to end soon, reputational damage has been done. People are fleeing the area, as images of smoke filled skies fill screens.

This will inevitably dampen foreign direct investment in the immediate future. The course and duration of the conflict will determine the degree to which the region can bounce back and continue to attract holidaymakers and young professionals and those seeking a life with more sun and less tax.

From a geopolitical perspective, the region’s recent success – aside from its vast and easily extracted natural resources – has rested largely on the assumed political stability that was underwritten by hosting US military bases and buying US military hardware. Both of these could now prove to be an economic liability.

The UAE and Saudi Arabia are now in blatant competition with one another. Competition is healthy, many will contend and this can be true but, if and when the times are more difficult such competition could become cut throat.

According to Abuamer and Nassar (2023), “soft power acquisition can also be used to explain how Gulf states approach sports.” Soft power, as Nye (2004) set out explain how some states acquire influence in non-confrontational ways and that sports investments can be explained by intra-Gulf rivalries, where competition rather than cooperation between Gulf states is arguably a key driver.

Competing for football glory; especially in the English Premier LeagueSaudi Arabia owns Newcastle United F.C.The Emirate of Dubai sponsors Arsenal F.C.The Emirate of Abu Dhabi both own and sponsor Manchester City F.C.

In 2018, The Economist explained the following in a piece with the following bi-line “An oasis for the tax-averse beckons in the Middle East”

More than 100 countries have signed up to the Common Reporting Standard (CRS), which requires them to swap information on account-holders that may be relevant for tax purposes. But the enterprising and tax-shy can still exploit loopholes in the system. A popular one is to procure residence in the United Arab Emirates (UAE), set up a company there and use the tax residence that comes with it to block the flow of information to tax authorities elsewhere. … Under the CRS (which is managed by the Organisation for Economic Co-operation and Development), banks must share information with the country where an account-holder is tax-resident. If the account holder is an entity, then the bank must look through it to the “controlling person” and report on that individual. In the UAE, since both the individual and the company have local tax residence, neither need fear having any information passed on to other countries, regardless of whether their money is held in a bank account, a trust or an investment fund.

Add to this that the UAE is largely tax-free and is likely to have to remain ‘mostly’ tax-free to retain its advantage over Saudi Arabia.

The Arabian peninsular seeks to become a default holiday destination

Its not just Dubai anymore.

Destination DohaDrift by Dhow; the Gulf’s once ubiquitous sail boats whose name may have come from the Persian for “small ship” (dawah) or from the Swahili for “vessel” (daw)

No longer just for pilgrimsLots to see, e.g., the UNESCO Al-Hijr monuments that date back to Nabataean civilizationTablet magazine in Jeddah, Saudi Arabia (Photo: Andrea Bruce)

And while it is no longer ‘just’ Dubai, it, Abu Dhabi and most other of the seven Emirates are all vying for tourists. It is said that the UAE will soon have a number of casinos. As it stands, and as I wrote recently, the UAE is the Middle East’s most popular destination be it as a conference location, convention centre or indeed holiday destination (Rutledge, 2023; 2024).

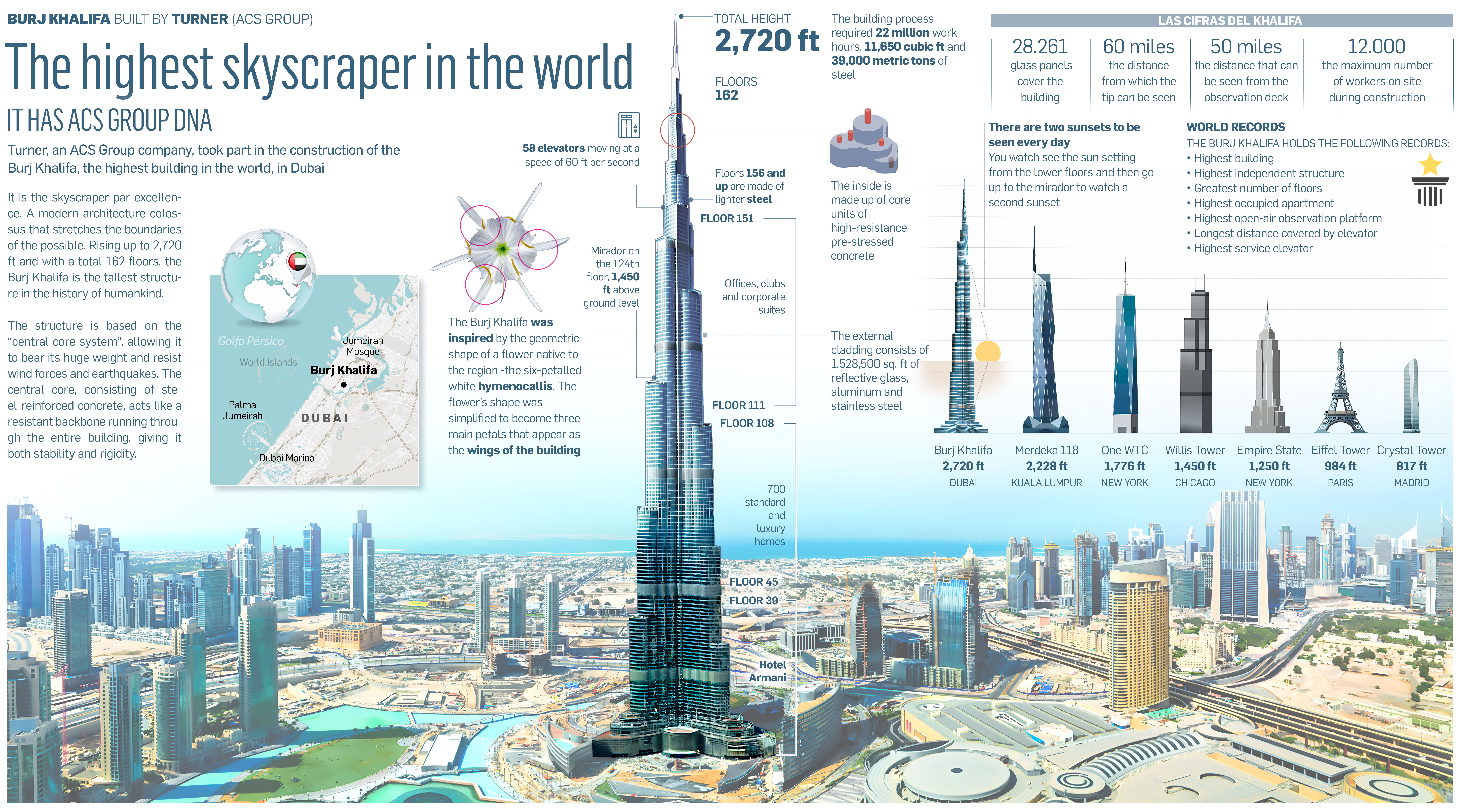

Some 21.5 m tourists visited in 2019 (UNWTO, 2023), a striking number considering that there are only around one million Emirati citizens (see: Arabian Gulf data). The meteoric growth in visitors is largely due to a proactive government strategy of infrastructural investment and destination brand-building (see, e.g., Chen and Dwyer, 2018). As Thani and Heenan (2017) state, in order to attract tourists the UAE has undergone some, “eye-catching transformations.” Notable amongst the cultural zones and theme park hubs are the world’s tallest structure (Burj Khalifa), biggest mall (The Dubai Mall), only seven-star hotel (The Burj Al Arab) and a satellite branch of France’s Louvre museum (Wippel, 2023). State controlled oil rent has facilitated the creation of two of the world’s largest airlines and airport hubs—Emirates and Etihad (DXB and AUH). In terms of marketing the UAE as an “escape to the sun” location, London’s English Premier League football club Arsenal, wear Emirates shirts and play home games at “Emirates stadium;” Manchester City wear Etihad shirts and play their home games at “ Etihad stadium” (Millington et al., 2021).

Chen, N., & Dwyer, L. (2018). Residents’ Place Satisfaction and Place Attachment on Destination Brand-Building Behaviors: Conceptual and Empirical Differentiation. Journal of Travel Research, 57(8), 1,026–1,041. https://doi.org/10.1177/0047287517729760

Millington, S., Steadman, C., Roberts, G., & Medway, D. (2021). The tale of three cities: Place branding, scalar complexity and football. In D. Medway, G. Warnaby, & J. Byrom (Eds.), A Research Agenda for Place Branding (pp. 131–149). Edward Elgar Publishing. https://doi.org/10.4337/9781839102851.00017

Rutledge, E. J. (2023). The tour guide role in the United Arab Emirates: Emiratisation, satisfaction and retention. Tourism and hospitality research, 23(4), 610–623. https://doi.org/10.1177/14673584221122488

Rutledge, E. J. (2024). The tour guide profession: An attractive option for UAE nationals majoring in tourism? Tourism and hospitality research, 0(online first), 1–12. https://doi.org/10.1177/14673584241278451

Thani, S., & Heenan, T. (2017). The UAE: A Disneyland in the desert. In H. Almuhrzi, H. Alriyami, & N. Scott (Eds.), Tourism in the Arab World: An Industry Perspective (pp. 104–117). Routledge. https://doi.org/10.4324/9781315624525

Wippel, S. (Ed.) (2023). Branding the Middle East: Communication Strategies and Image Building from Qom to Casablanca. De Gruyter. https://doi.org/10.1515/9783110741100

Qatar has over the past three decades mediated several high-profile conflicts that have brought it unparalleled attention. It’s been said that this is remarkable given the commonly accepted assumption that small states, particularly from the Global South, are inherently limited in their power to act as third parties during conflict (Barakat, 2024). Qatar’s rise as a mediator didn’t happen overnight. According Wirtschafter (2024), Qatar started to play a regionally important role in the years after the the launch of Al Jazeera, “which gave the small Gulf state an outsized influence” .

Qatar’s emir, Sheikh Tamim bin Hamad Al Thani. Qatar is winning praise for its diplomacy skills. Vyacheslav Prokofyev/AP

Qatar’s strategic importance is further reinforced by its hosting of Al Udeid Air Base, the largest U.S. military installation in the region, and the presence of six major U.S. universities at Doha’s Education City.

A car sticker supports Qatar’s relationship with Turkey, which has deepened as a result of the blockade. Naseem Zeitoon/Reuters

“Al Jazeera helped create Qatar’s maverick image but also repeatedly got it into hot water. During the Iraq War, President George W. Bush, in a meeting with British Prime Minister Tony Blair, reportedly contemplated bombing the Doha headquarters of the broadcaster, which was airing video of the fighting in the Iraqi city of Fallujah that the Pentagon said was misleading. The White House dismissed the report at the time, and the British government denied it.”

As Kamrava (2012) wrote, across the Arabian Gulf “an authoritarian retrenchment and narrowing of political space has emerged.” This reassertion of the state’s dictatorial authority has, of course, taken different forms across the region depending on the state’s overall societal posture. In Qatar, for example, where anti-state sentiments are conspicuous in their absence, there have not been any discernible changes in the domestic political environment. In the UAE, however, the space provided to civil society organisations has been steadily narrowed by the state since the beginning of the regional unrest. In Bahrain and Saudi Arabia, repression was notably more draconian still.

Abouzzohour (2021) ponders what are the implications of the fact that no monarch was overthrown during or since the Arab Spring. Various experts have linked the latter to monarchs’ legitimacy, external support, and resource wealth. She suggests that while there is no consensus view, “it is clear that monarchs have repeatedly and successfully contained different types of opposition threats for decades prior to the Arab Spring and continue to do so 10 years later.”

The “Arab Spring”The Economist (2020). Expand map.

Ten years on from the “Arab Spring” The Economist (2020) write:

“What kind of repression do you imagine it takes for a young man to do this?” So asked Leila Bouazizi after her brother, Muhammad, set himself on fire ten years ago. Local officials in Tunisia had confiscated his fruit cart, ostensibly because he did not have a permit but really because they wanted to extort money from him. It was the final indignity for the young man. “How do you expect me to make a living?” he shouted before dousing himself with petrol in front of the governor’s office. His actions would resonate across the region, where millions of others had reached breaking-point, too. Their rage against oppressive leaders and corrupt states came bursting forth as the Arab spring. Uprisings toppled the dictators of four countries—Egypt, Libya, Tunisia and Yemen. For a moment it seemed as if democracy had arrived in the Arab world at last. … Only one of those democratic experiments yielded a durable result—fittingly, in Bouazizi’s Tunisia. Egypt’s failed miserably, ending in a military coup. Libya, Yemen and, worst of all, Syria descended into bloody civil wars that drew in foreign powers. The Arab spring turned to bitter winter so quickly that many people now despair of the region. Much has changed there since, but not for the better. The Arab world’s despots are far from secure. With oil prices low, even petro-potentates can no longer afford to buy their subjects off with fat subsidies and cushy government jobs. Many leaders have grown more paranoid and oppressive. Muhammad bin Salman of Saudi Arabia locks up his own relatives. Egypt’s Abdel-Fattah al-Sisi has stifled the press and crushed civil society. One lesson autocrats learned from the Arab spring is that any flicker of dissent must be snuffed out fast, lest it spread.

The London-based magazine concludes that, “The region is less free than it was in 2010—and perhaps [now even] more angry.”

Dubai epitomises the Gulf’s property market. It did suffer a massive correction back in 2009 (Collinson, 2009), the Emirate needed to borrow several billion from Abu Dhabi (Davidson, 2009) but, that debt has been repaid and today the sector is once again booming (Maccioni, 2024).

The following was penned by Davidson in 2009; at the tail-end of the 2003–2008 period in the Emirate of Dubai (UAE) which was described by Bertrand (2012) as “the world’s most massive real estate bubble.”

Glitzy Dubai, long considered the new Monte Carlo or the Las Vegas of the Middle East, has suffered one of the worst crash landings of this global recession. Dubai might be considered a bellwether of the global credit crunch. Until recently touted as a beacon of progress in an otherwise unstable region, the tiny emirate’s seemingly innovative economic and political model is now unravelling, with no end in sight to the uninterrupted stream of bad news. Construction has ground to a shuddering halt, unemployment is rising, sovereign debt is exposed, lawsuits are being prepared, and the population is decreasing, as those who moved to Dubai in search of a better life have either lost their jobs or are cutting their losses and leaving. To make matters worse, as the city empties itself out, traffic thins, and cars and credit cards are abandoned at the airport, the embattled authorities have embroiled themselves in fresh controversies by introducing protectionist policies for their citizens and a new media law that forbids criticism of the economy, and earning Dubai an anti-Semitic branding in the sports world by denying a visa to an Israeli athlete. With investor confidence in tatters and debt repayments looming, its humiliated rulers have had little choice but to turn to their wealthier neighbors. But although help has finally arrived, it is by no means the lifeline that the emirate really needs, and Dubai’s future hangs in the balance.

Only time will tell for history is history (unendingly so). The digitisation of everything is as good as it is bad. One’s predictions and forecasts, with hindsight and internet indexing, can come to be seen as having been too hubristic (one could counter that they were just thinking and writing in a heuristic fashion).

In the same year as Davidson wrote the above, Lewis (2009) said the following. “A six-year boom that turned sand dunes into a glittering metropolis, creating the world’s tallest building, its biggest shopping mall and, some say, a shrine to unbridled capitalism, is grinding to a halt.” And that, “half of all the UAE’s construction projects, totalling £400 billion, have either been put on hold or cancelled, leaving a trail of half-built towers on the outskirts of the city stretching into the desert.”

Red hot (once more)

In a recent piece for the London-based Financial Times, it was said that if you want to “escape the global gloom, just take a flight from its epicentre, London, to any leading capital of the Gulf” Sharma (2022). “Dubai is enjoying yet another real estate boom. Regional rivals like Riyadh are racing to be the next Dubai, funnelling oil profits into property mega-projects.” Sharma also suggests that many of the Gulf leaders do “recognise that a boom built on high oil and property prices is unlikely to endure, but that age-old problem can wait.”

In 2023 The Economist wrote that while Dubai’s property market has much to recommend it (low taxes and a large pool of renters), some wonder if the sector, “the backbone of Dubai’s economy, is again becoming a bubble.” The Emirate has already endured two real estate crashes this century: “an abrupt one during the financial crisis in 2008, when property values fell by half, and a slower one from 2014 to 2020, when they slid by 35 per cent.”

Hanieh, A. (2018). Money, Markets, and Monarchies: The Gulf Cooperation Council and the Political Economy of the Contemporary Middle East. Cambridge University Press.

Renaud, B. (2012). Real Estate Bubble and Financial Crisis in Dubai: Dynamics and Policy Responses. Journal of real estate literature, 20(1), 51–78. https://doi.org/10.1080/10835547.2012.12090313

Oil continues to influence global economics and politics like no other finite natural resource. In the 2024 US presidential election, the strategic commodity will be an important domestic issue.

As the biggest producer and consumer of oil on the planet, the US has a particularly strong relationship with the black stuff. And the candidates know it.

Meanwhile, Joe Biden has attempted to reduce dependence on fossil fuels with his green energy policy and other legislation. Yet at the same time he has overseen an increase in domestic oil production and promised motorists he will keep petrol prices low.

It’s an important promise in the US, a country whose love affair with cars is well known. Out-of-town shopping malls, long highways and a lack of government investment in public transportation have fuelled car dependency, with many cities being designed around huge road systems.

So it is perhaps unsurprising that pump prices are a significant factor influencing voters. Research has even shown that gasoline prices have an “outsized effect” on inflation expectations and consumer sentiment. As fuel prices go up, confidence in the economy goes down.

And while many European and Asian countries have shifted towards alternative energy sources, the US has not reduced its dependence on fossil fuels when it comes to transport. Electric models make up only 8% of vehicles sold in the US, compared to 21% in Europe and 29% in China.

Any rise in gasoline prices ahead of the US summer “driving season” – when holidays and better weather encourage more road travel and gasoline consumption is estimated to be 400,000 barrels per day higher than other times – would be a serious concern for the Democratic party.

Yet it’s also true that whoever is in the White House actually has limited ability to influence gasoline prices. Around 50% of the pump price is the cost of crude oil, the price of which is set by international markets.

And despite producing enough oil domestically to cover its consumption, the US continues to trade its oil around the world. Back in 2015, Congress voted to lift restrictions on US crude oil exports that had been in place for four decades, allowing US companies to sell their oil to the highest international bidder.

To complicate things further, some US refineries can only deal with a certain type of crude oil, which has to be imported. Neither international events or foreign production decisions are under the control of a US president.

Indeed, oil price spikes caused by political crises in other oil producing regions illustrate how continued dependence on oil itself, whether domestically produced or imported, leaves the US exposed to global market shocks which could in turn influence electoral outcomes.

After Russia’s full scale invasion of Ukraine in 2022 and production cuts from countries such as Saudi Arabia in 2023, the Republican party used a rise in gasoline prices to attack Biden’s environmental policies which had reduced domestic oil drilling and ended drilling leases in the Arctic.

Big oil, little oil

So while the US president has little say over the price of fuel that voters pay, domestic oil and gas regulations have a role to play, as oil producers make up a significant body of influence in the US.

Aside from the big firms backing Trump, the structure of the US oil industry is unique among oil producing states in that it is dominated by a very large number of small independent producers who earn money from the extraction and sale of oil from their land.

Some campaigners have blamed Biden for price rises at the pump

In most oil-producing countries, subsurface oil is owned by the state. But in the US, the mineral rights are owned by the private landowner who can earn royalties by allowing oil companies to drill on their land. In 2019, there were 12.5 million royalty owners in the US. Operating alongside them are some 9,000 independent fossil fuel companies which produce around 83% of the country’s oil and account for 3% of GDP and 4 million jobs.

Those companies drilling on state-owned land pay a royalty rate to the government, which up until recently was as low as 12.5% of the subsequent sales revenue. Biden’s decision to raise the rate to 16.67% did not go down well with oil producers.

Surging US oil production may help with the Democrats’ re-election bid, but rising gasoline prices will not – even though their levels depend on much more than Biden’s energy policies. Instead, it may be that the international economics of oil markets drive voters’ decisions – and determine who wins and who loses in November 2024.

It looks like an image from science fiction: a 262m-tall lighthouse-style tower rising from the centre of hundreds of concentric circles of shining panels. But, if all goes to plan, these ambitious design renderings will become science fact, as the fourth development phase of Dubai’s colossal $14bn solar power park.

VirtualRealitySheikh Mohammed bin Rashid, Vice President and Ruler of Dubai, at the MBR Solar Park (24 November 2020)That’s 10,943,945,000 pounds sterling (£).

Images @ Dubai Electricity and Water Authority

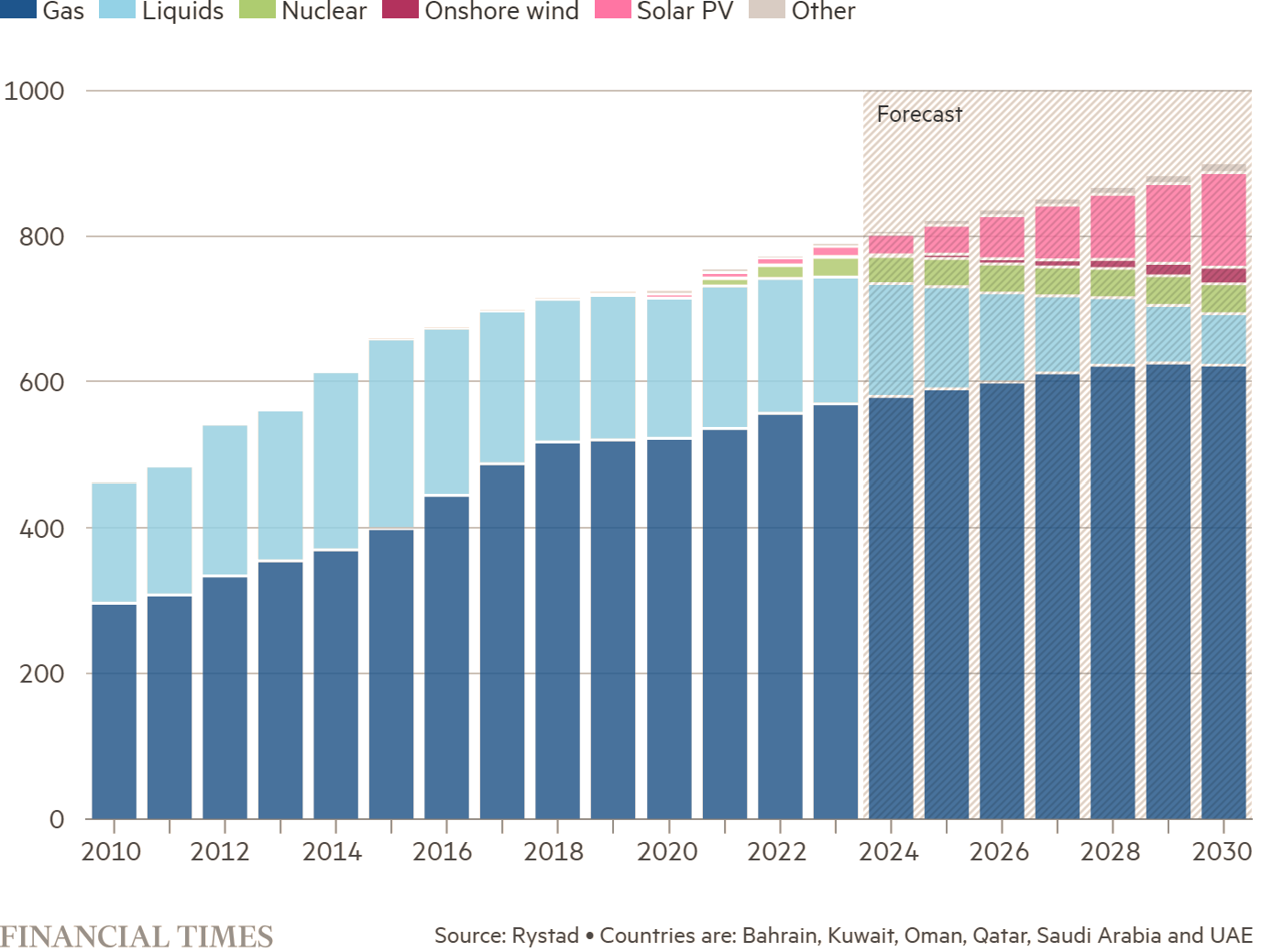

In the fossil fuel-rich Gulf, however, the Mohammed bin Rashid al-Maktoum Solar Park, as it is known — which was begun in 2013 and is largely up and running — remains an outlier. Overall, the region’s renewable energy investments have lagged behind China, the US and Europe.

In its 2024 report on energy investment, published this month, the International Energy Agency said the broader Middle East, including countries such as Iran and Iraq, was allocating just 20 cents to renewable energy investment for every dollar spent on fossil fuels — or one-tenth of the global average. The IEA added that, of the $175bn the region was expected to invest in energy projects this year, just 15 per cent would go to clean energy.

The oil and gas reserves sitting below the Gulf states have previously discouraged any rapid development of renewables. “The Gulf countries are blessed with a vast amount of resources of oil and gas,” notes Aisha al-Sarihi, research fellow at the National University of Singapore’s Middle East Institute. “That has made access to energy very affordable … and eliminated the need for alternatives.”

Electricity was previously powered by oil in large part. But downward pressure on oil prices from increased US shale oil triggered a shift in the mid-2010s, making gas and renewables more viable as more oil supplies were reserved for export, says Karen Young, chair of the Economics and Energy Program Advisory Council at the Washington, DC-based Middle East Institute.

During that period there was a “ramping-up of the kind of fiscal-side reforms on spending”, says Young, and the “beginning of talking about reduction of subsidies of gasoline, of electricity prices, water prices”.

Even as the wealthy Gulf nations have become more aware of the need to decouple their economies from oil, the United Arab Emirates’ hosting of the COP28 climate meeting last year encapsulated the paradoxes that surround the Gulf states’ role in the energy transition.

On the one hand, the Dubai COP ensured that producer countries were at the centre of the negotiations, with oil-rich emirate Abu Dhabi — the UAE’s capital and centre of political power — wanting to expand fossil fuel production. On the other, Dubai, for the first time, secured a deal to transition away from fossil fuels, and the UAE set aside $30bn for a “catalytic climate investment fund”.

Although the transition from fossil fuels in many industries could theoretically reduce demand for crude oil, the Gulf states do not view this as an existential threat to their revenues.

“The producers in the Gulf see a different scenario — and particularly a lifeline through petrochemicals — [in which] there will be sustained demand for their product for at least the next 20 years,” says Young.

The Gulf states “believe they will be the last man standing because they will sell the lowest carbon intensity fuel in the future”, adds al-Sarihi, on the basis that compared with other sources of oil, those in the region require the least amount of energy to extract.

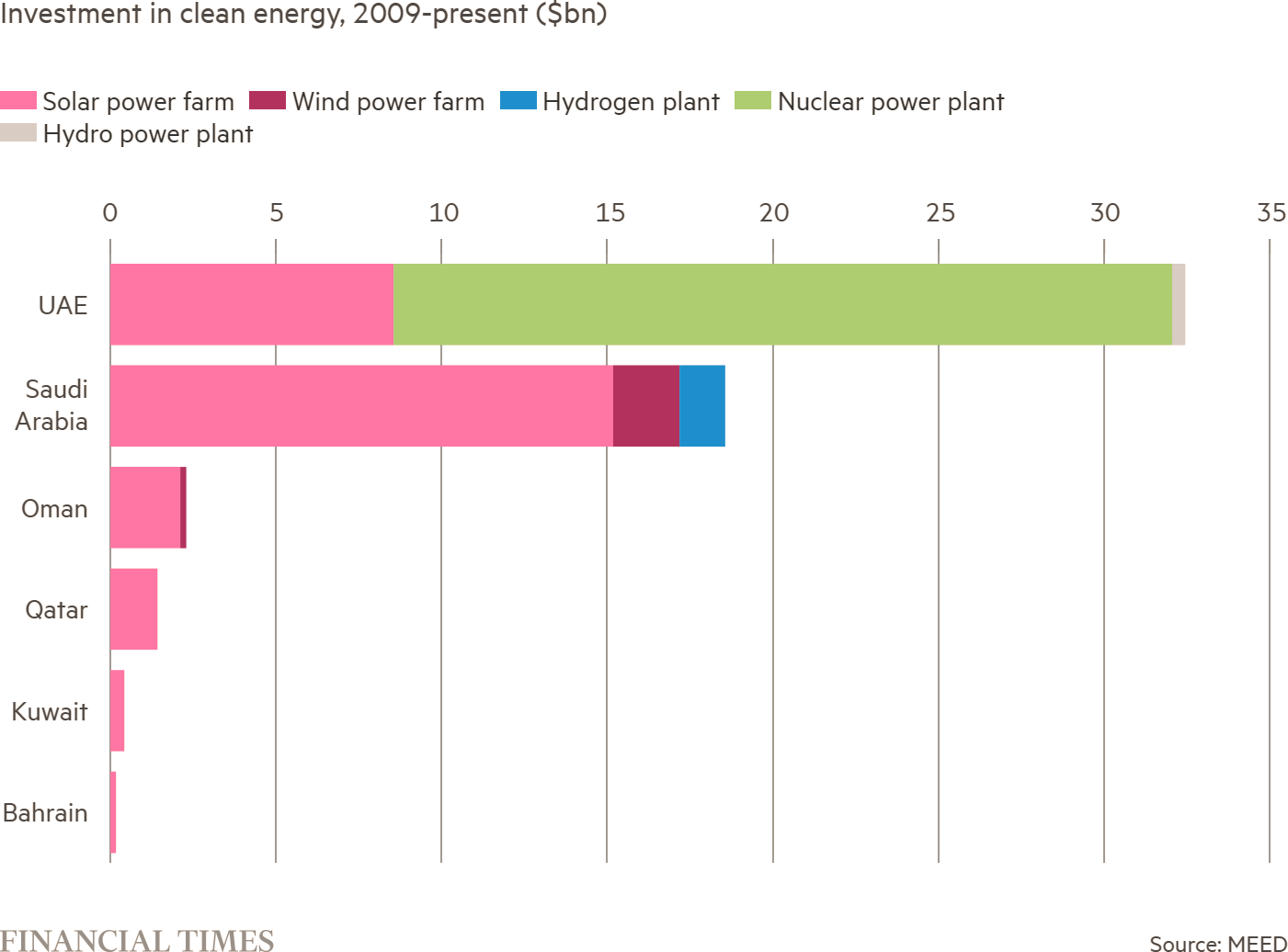

However, at the same time, economics and strategic interests are galvanising petrodollar-financed renewable energy investments by the Gulf. This spending is led by the UAE and Saudi Arabia, which are actively working to diversify their economies and reduce their dependence on fossil fuels.

The Gulf states have a “dual approach” to the energy transition, according to al-Sarihi. “One is to continue with the fossil fuel industry and … invest in clean energy technologies and other resources like hydrogen,” she says.

“The Gulf states are taking advantage of the international arena when it comes to the energy transition,” adds al-Sarihi. “They use it as a platform to exert their energy diplomacy and influence in a way that makes the energy transition serve their interest … they try to secure a market for their energy supplies. They are now pivoting to Asia because it is becoming the centre of demand for energy.”

But the autocratic states are not investing very widely across the energy transition, points out Robin Mills, Dubai-based chief executive of consultancy Qamar Energy. There has been scant movement towards decarbonising in transport or industrial sectors, for example. “The real investments have been around the power sector — solar and nuclear,” Mills says.

For example, the UAE’s Barakah nuclear plant will meet up to a quarter of the country’s electricity needs by the time all four of its reactors are fully operational. And, in Saudi Arabia, while just 0.2 per cent of the electricity was generated by renewables in 2022, according to US government statistics, solar power plants have been built, including the 1.5GW capacity Sudair.

The Gulf states are also investing in clean power in other countries, from central Asia to central Africa. Young highlights Masdar, Abu Dhabi’s renewable energy investment vehicle, and Saudi’s national champion ACWA Power as “two of the most important power developers in emerging markets in the world”.

“They’re competing and partnering with the biggest infrastructure investors in the world, she observes. “They’re doing this in ways that I think have enormous soft power, political influence.”